Total return reinsurers at a crossroads

New-breed companies need to pivot to become relevant and sustainable.

Total return reinsurers will increasingly have to rethink their strategies after initially struggling to make much of an impact on the global reinsurance market.

“They are facing some challenges,” Carlos Wong-Fupuy, a Senior Director at AM Best, told a virtual press briefing. “Investment volatility given their investment strategies has been a bit disappointing, some companies are trying to re-evaluate their investment strategies, they’re trying to remodel themselves, they’re having some changes in top management.”

Some of these start-ups are pivoting away from their original business models, having struggled to make headway in a reinsurance market in which investment returns are meagre and clients are increasingly shifting to work with large reinsurers.

“They are going through a metamorphosis,” said Anthony Diodato, a Best Managing Director. “If you look at Hamilton, they were going down one path, and just recently they acquired Pembroke. They are changing their business model. Sirius has been around for 75 years and has an established track record. Third Point has maybe had a little trouble with getting market momentum, just being a follower in the marketplace. They’re coming together. So, [total return reinsurers are] evolving. That’s not to say that one is better than another, but [they will] morph over time as they decide which way they want to go.”

Total return reinsurers’ have had a rocky ride, according to recent Best’s research. The agency found that a composite of five of these companies that have operated for at least the past five years have performed much worse than their established Bermuda rivals. They had an average five-year combined ratio between 2014 and 2019 of 111.2%, compared with 98.4 for the Bermuda reinsurers. Total return reinsurers’ return on equity has also been very disappointing, with a five-year average of -0.3%, the agency found.

Their poor performance seems to be due to their higher loss and expense ratios, driven partly by the large amount of medium-term casualty business they’ve underwritten, and because they lack the established track records of the Bermuda reinsurers, Best said.

More M&A among the total return players might be in the pipeline. “I think this is an evolving space,” said Wong-Fupuy. Arch Capital is reportedly leading a consortium that has made a $500m bid for Watford Holdings. Arch is Watford’s largest shareholder, as well as carrying out its underwriting.

Maintains stable outlook

AM Best has maintained its stable outlook on the global reinsurance industry, unlike its rival S&P which recently dropped its view to negative.

“We’re not saying there aren’t difficulties that the global reinsurance sector won’t face over the near term,” Stefan Holzberger, AM Best’s Chief Rating Officer (pictured above), told the briefing. “But, we do feel it is well-positioned to handle those challenges and we’re seeing a positive trend in some very meaningful aspects, such as the pricing environment and an adjustment of the terms and conditions.”

These and other “tailwinds” – including increasing confidence that the COVID-19 bill will be manageable and a rapidly hardening primary insurance market that is feeding through to reinsurance – will, Best believes, cancel out the headwinds facing reinsurers, such as low interest rates, capital market volatility and less cushion in their reserves.

The stable outlook reflects the “new normal,” said Wong-Fupuy. “The market is having to get used to levels of performance that are below the historical levels we were used. But, the market is relatively stable.”

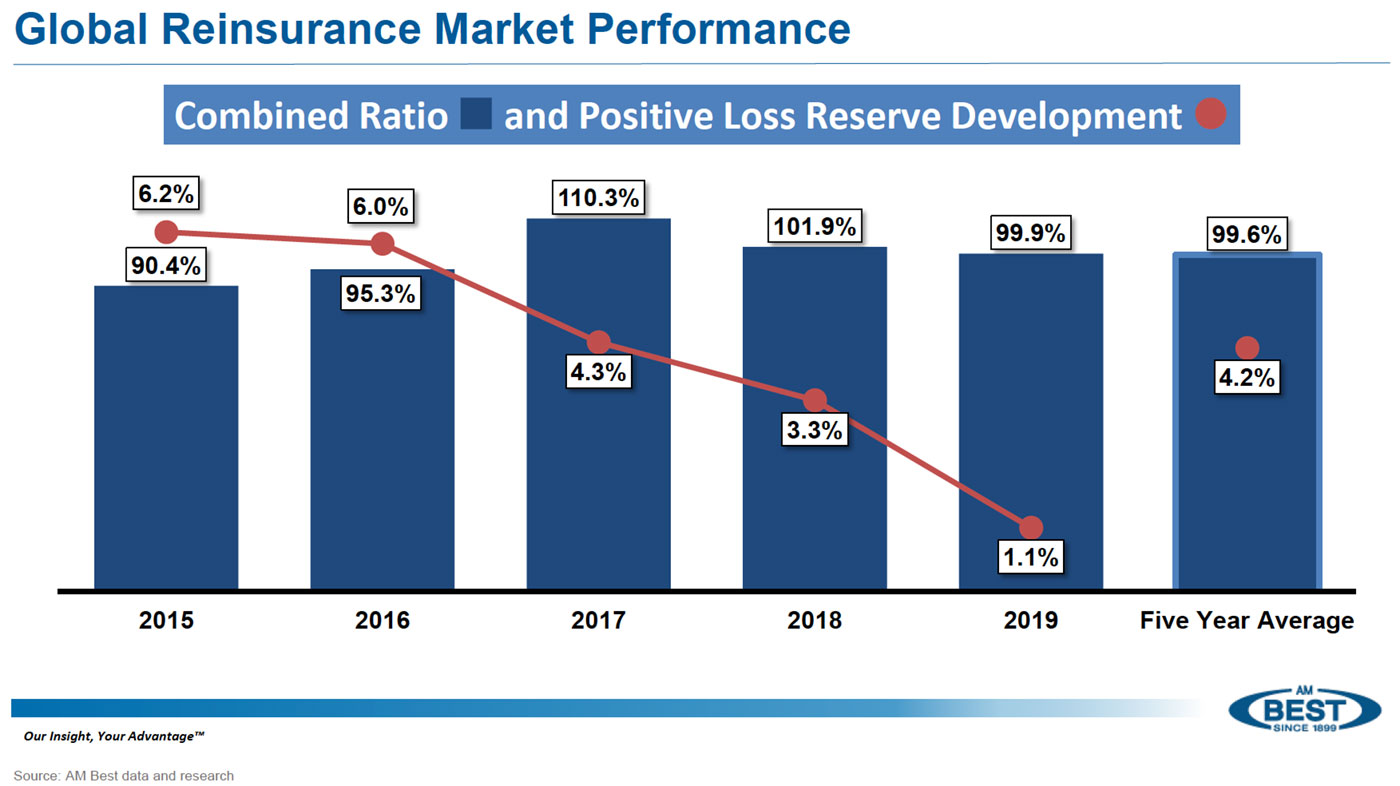

Weaning itself off reserve releases

AM Best detailed the extent to which the reinsurance industry has relied on reserve releases to boost its performance. They helped boost the industry’s combined ratio by an average of 4.2% over the past five years, enabling it to post an average combined ratio for that period of 99.6% – an underwriting profit, if only just. Reserve releases also added 3-4% to the industry’s return on equity. Without them, its five-year average return to 2019 was just 3%, Best’s said.

“The amount of reserve releases in recent years has continued to surprise us. It’s had a positive impact on underwriting results for many years,” said Greg Carter, its Managing Director, Analytics. But, he added: “the well is running dry.”

Reinsurers remain cautious that the COVID-19 insured loss could still jump, meaning they will think twice in future about releasing what few excess reserves they have left, said Wong-Fupuy. That dwindling pot of windfall profit, however, will help strengthen reinsurers’ resolve to push up their prices and tighten what have been generous terms and conditions. “In a low interest rate environment, there is no other source of profits apart from improving underwriting discipline,” Wong-Fupuy added.

Simon Challis is a contributing editor to Reactions